One of the biggest financial stories of 2021 was probably the one about rising bond yields. The other biggies were inflation and supply chain disruptions. But a close look at the data shows that maybe those three are one, viewed through three different vantage points. Whatever the reason, since yields hit some recent highs, the topic is top of mind and now is a good time to sort it out.

When yields on something like 10-year treasury bonds rise, experts debate about the cause. Maybe it’s because the economy is growing and bonds have to offer a higher yield to compete with the higher returns available by investing in growth-sensitive investments, like stocks or real estate. Maybe it’s due to inflation, and bonds need to compensate investors not just for the loss of the use of their money for 10 years, but also for the loss in purchasing power each year. Maybe it’s the central bank, which might switch from pushing interest rates down to pulling them up. Maybe, at least outside of the most trusted economies, it’s the risk of default, though that doesn’t seem to have much effect in the U.S. context.

How is one to know which effect is present at which time? Well, common sense suggests that bond investors are watching all of these factors and that, in some sense, they are all affecting yields to one degree or another, either by changing or by not changing. In other words, a belief that inflation will not change still affects yields, but it does it by not changing the part of the yield which reflects inflation risks. To borrow from the fictional Sherlock Holmes, sometimes the fact that the dog didn’t bark is a piece of evidence too.

So, how might we study bond yields to see which factor or factors are the main driver of, for example, increases in 10-year treasury yields?

We do it not only by seeing that investors are selling those bonds, but also by looking at what they are buying with the proceeds of those sales. When yields are rising, that means there is less demand for bonds relative to supply. It means that, all other things being equal, investors are more willing to sell the bonds they own or less willing to buy more. That makes bond prices lower than they would be if demand were high, and since yields are calculated by putting the price of the bond in the denominator, a lower price means a higher yield. Sometimes the financial press “explainers” say that lower prices cause higher yields, but that’s a little confusing. Lower prices simply are higher yields. If you take the fraction 1/2 and change the denominator to 4, you get 1/4th, which is smaller. There’s no cause and effect here, just pure mathematical identity.

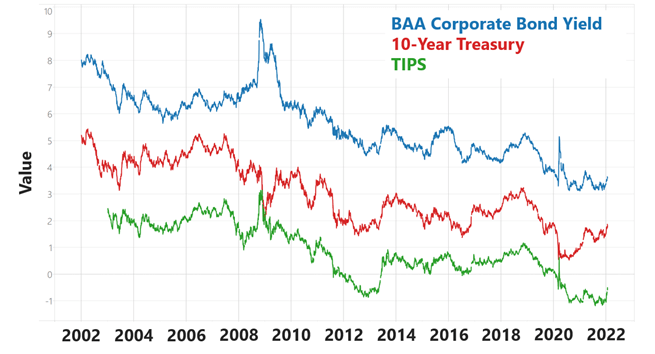

So, if demand for 10-year treasuries goes down, all other things being equal, yields go up. But we don’t know why demand went down if we just make guesses in a vacuum. We have to look at what the demand shifted to. If people sell a lot of treasuries, we only know a small part of the story until we find out what they bought with that money. Maybe they used the proceeds to buy riskier but higher-yield corporate bonds. That could be a sign of optimism about growth and about corporate bond default rates.

Or maybe they sold regular treasury bonds and bought inflation-protected bonds (or Treasury Inflation-Protected Securities (TIPS)). That points towards inflation fears as the reason for the rise in rates.

Here’s a chart that shows those three yields together:

So, the shift in these yields relative to one another tells the other half of the story. What investors buy instead of treasuries tells us what they are frightened of or where they believe there is opportunity. Next, we’ll look at some of those yield spreads to see what knowledge they’ll yield up.